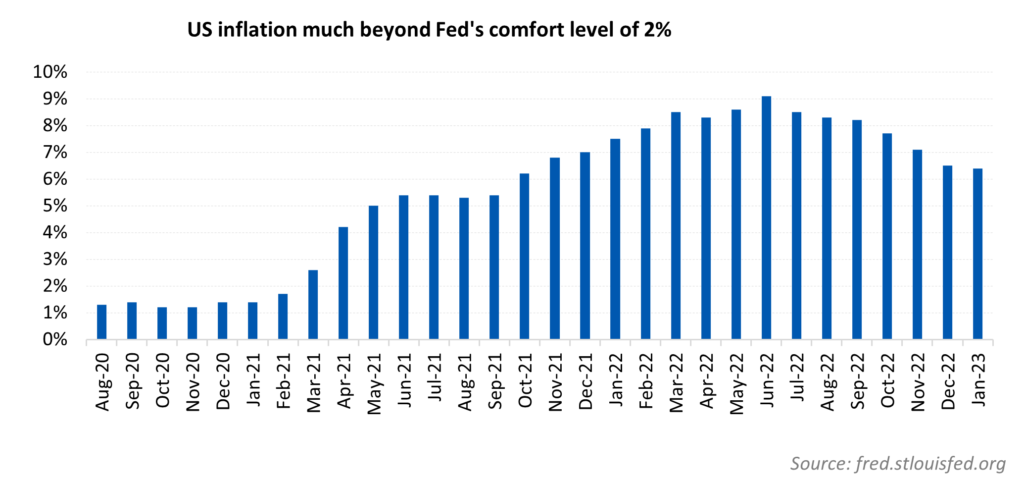

A sudden rise in inflation in 2021 prompted the Federal Reserve to tweak its monetary policy outlook. The Consumer Price Index increased 7% in 2021 and peaked at 9.1% in June 2022, the highest since 1981. Though the CPI started to trend lower at the end of 2022, it was still way higher than the Fed’s target of 2% over the long term.

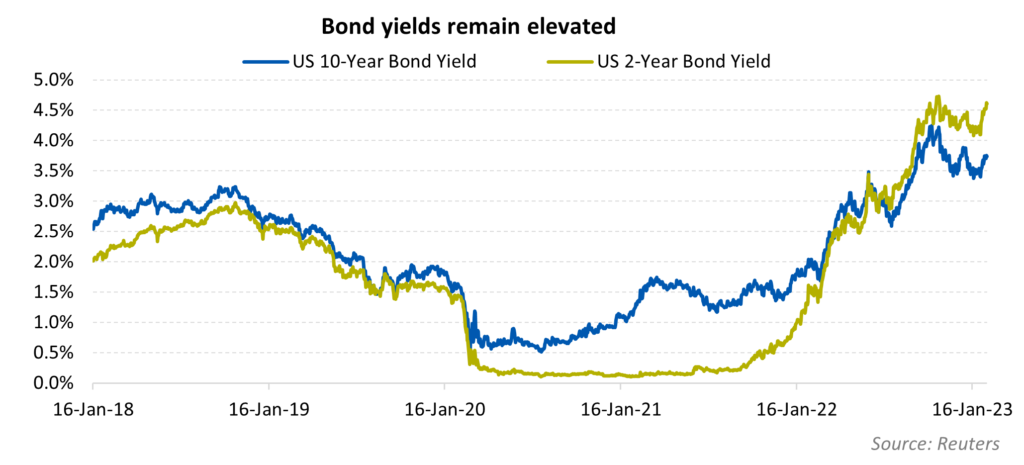

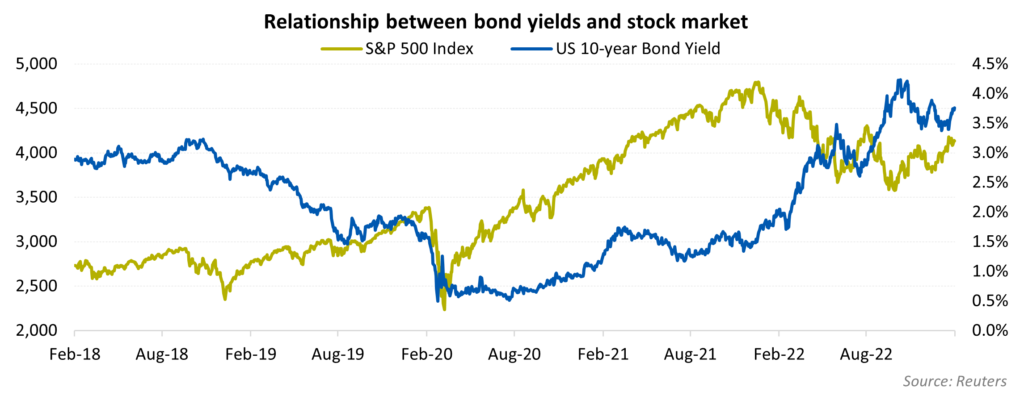

In response, the Fed raised interest rates eight times in a row, from March 2022 to the present. Fed rate is the benchmark rate that banks levy on each other for overnight borrowings and it also has spill- over effects on numerous consumer debt products. Changes in the bond market reflected the Fed’s revised policy stance. Yields on the benchmark 10-year US Treasury Note increased from 1.52% at the end of 2021 to more than 4% in October 2022 and is currently around 3.8%. The peak rate was the highest in more than 10 years. Yields on 2-month US Treasury Bills, with direct correlation to the Fed rate, inched up from 0.10% in February 2021 to a peak of 4.73% in November 2022. Higher bond yields have an adverse impact on equities due to the negative correlation between the two.

Impact on equities

Opportunity cost: Equities become unattractive with a rise in bond yields unless returns are better than the combination of bond yields and equity risk premium. Therefore, the opportunity cost of investing in equities goes up with an increase in bond yields, thus making them less appealing.

Cost of capital: Rise in the cost of capital can lower corporate earnings due to higher debt servicing costs. Additionally, companies refinancing debt have to pay higher interest charges owing to the increasing cost. Subdued corporate earnings could compress valuation of stocks.

Higher discounting factor: This is another reason for underperformance of stocks in a rising interest rate environment. Higher bond yields reduce the current value of corporates’ future earnings due to an expansion in the discounting factor. Stock prices are susceptible to downward pressure on weakening earnings growth.

In a higher interest rate scenario, worst-hit stocks are arguably those with high P/E multiples. Stocks that are elevated from a valuation perspective can suffer considerable price erosion.

For stocks to become the preferred alternative, investors should be compensated for the additional risks taken, either through higher coupons or strong earnings growth. Headwinds exist for global economic growth and the recent geopolitical tensions, labour shortages (can fuel inflation) and supply chain issues, arising from reshoring, will likely pose challenges for the stock’s valuation expansion.

Considerable increase in borrowing costs has already dented housing activity, and strengthening of the US dollar (still at an elevated level despite the recent fall) is an overhang on the profitability of US corporates. As per IBES data from Refinitiv, Q4 FY22 earnings of S&P 500 companies (that have reported earnings so far) have declined 2.8% YoY, while profit margins are being squeezed by inflation that has eroded the ability of corporates to pass on rising costs to consumers.

Credit Suisse estimates Q4 FY22 to be the worst earnings season outside of a recession in 24 years. The earnings outlook for the first half of FY23 is subdued as a strong labour market and rising borrowing costs continue to weigh on companies’ margins. The Fed has already hinted at a 25-basis-point hike at the upcoming meetings in March and May. The latest CPI number, which came in at 6.4%, is higher than the estimate of 6.2%, strengthening the view that the terminal rate could move up further from the current level.

The outlook for global GDP growth remains bleak since China is still not completely out of the Covid pandemic and the European energy crisis continues unabated. That said, there is no imminent risk of the world economy slipping into recession, at least in the first half of 2023. However, fundamentals are expected to worsen due to deterioration in financial conditions and the monetary policy turning out to be more hawkish for global growth to sustain at the current level. Higher bond yields and Fed’s tightening could induce sharp market volatility in the short term, thus resulting in a negative bias towards equities.

Author: Pravin Bokade, Director- Investment Research