The COVID-19 pandemic unleashed many challenges for the auto segment, the key concerns being decline in sales and shortage of semiconductors. While the growth momentum in order books is returning gradually, the short supply of semiconductors has compelled several OEMs to either shut shop or remodel products by eliminating certain key features, in their bid to cater to demand.

The gap between the demand and supply of chips has widened significantly over the last two years, with rising demand for consumer products running on chips aggravating the situation. Besides automotives, semiconductors are used in wireless and wired communication, PCs, storage, GPUs, peripherals, industrial, and consumer electronics. Sale of consumer goods and automobiles dropped significantly in 2020 but picked up in the second half of 2021. During the same period, demand for chips from the auto sector remained subdued, while that from the technology segment increased. Furthermore, the rise in remote working contributed to the growth in demand for wireless connectivity and PCs. Moreover, demand from the automotive segment started to recover once lockdowns eased, contributing to the shortage.

Amid the shortage of semiconductors globally, assembly line operations came to a grinding halt worldwide. Major car manufacturers and OEMs announced a cut in production that hit their revenues. During the pandemic, auto sales dropped around 80% in Europe, 70% in China and 50% in the US. Two other factors worsened the shortage: winter storms in the US resulting in the closure of chip manufacturing plants in Texas; and a major fire outbreak at chip manufacturer Renesas Electronics’ factory in Japan. Together these factories accounted for 50% of the semiconductor chips used in cars globally.

Capacity exhaustion

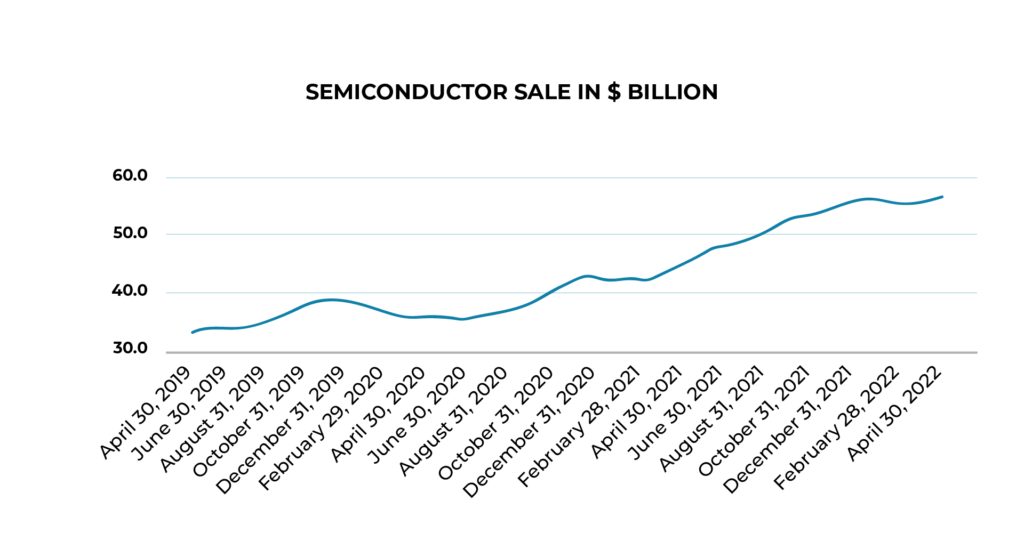

The semiconductor industry is growing at a robust rate in terms of revenues. However, capacity addition has failed to keep pace, lagging behind. Over the years, the industry has matured, with capacity growing around 4% annually. Utilisation, at or above 80% in the past decade, reached 90% in 2020. Although production has increased nearly 180% since 2000, total semiconductor capacity stands exhausted, given the high utilisation rate currently.

Impact of Russia-Ukraine War

The Russian invasion of Ukraine has put additional strain on existing supplies. Ukraine accounts for 25–35% of the supply of purified neon gas globally, while Russia caters to 25–30% of the demand for palladium, a rare metal used in semiconductors.

Stock piling and disruption in supply chain

Amid rising geopolitical tensions and regional disturbances within nations, consumer electronics manufacturers are resorting to stockpiling inventory as a hedge against potential supply disruptions. Due to stockpiling, prices have gone up by 5–10%. Moreover, semiconductors are largely transported by air. Therefore, an increase in the cost of transportation, amid the rise in fuel prices worldwide, has aggravated the situation.

Manufacturers usually resort to just-in-time (JIT) manufacturing, a widespread practice in the auto industry, to minimise waste and keep inventory levels low. However, the efficacy of JIT inventory management rests on accuracy of forecasts. In case of unforeseen shortages, the practice could severely disrupt the supply chain.

Impact of chip shortage on the auto sector

In 2021, due to the short supply of chips, the global automotive industry raked in just $200 billion in revenues. The demand for semiconductors from the auto segment in India totalled $24 billion at the beginning of 2022; it is expected to continue growing at a fast pace in the coming years.

Conclusion

Some of the large chip manufacturers in the US and Europe are expanding manufacturing capacities, which may aid recovery in the automotive industry from mid-2023. Investments in chip manufacturing in Southeast Asia are also likely to help in addressing the semiconductor shortage. In fact, chip giants in Taiwan and South Korea have earmarked significant investments for capacity expansion over the next few years. Many OEMs are adopting supply chain management technologies to leverage and forecast demand effectively. Moreover, several manufacturers are renewing contracts for a period of 15–18 months to efficiently cater to the demand. However, the current geopolitical environment and macroeconomic uncertainties globally, coupled with growing demand-supply gap, continue to pose concerns. In this scenario, it will take some time for the new processes and procedures (adopted by manufacturers) to address supply disruption-related issues effectively. Until then, for another couple of years or so, the shortage of semiconductors will continue to plague industries worldwide, especially the automotive segment.

Author –

Prasanth Radhakrishnan, Associate Director, Avalon Global Research

Contact us at https://www.agrknowledge.com/contact-us