By The Numbers: NICKEL – Metal of the Future!

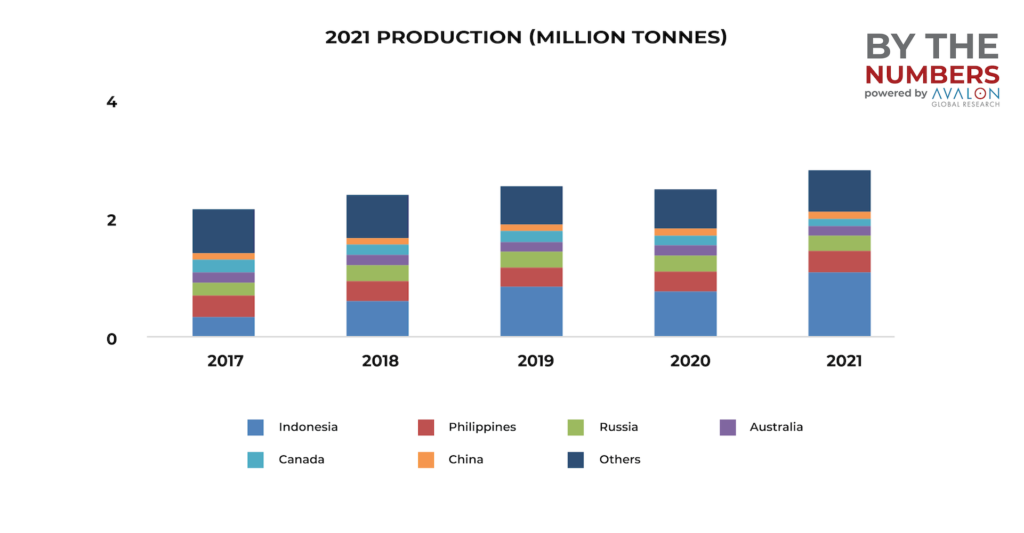

Growth in nickel’s mine output over the years

- The largest global nickel reserves are in Indonesia amounting about 20 million metric ton (mt), with Australia and Brazil following at 19 million mt and 15 million mt, respectively.

- Global nickel mine production has increased at a CAGR of 7.6% over 2017-2021, with Indonesia, Russia, and Philippines comprising over 55% of the global nickel output.

- Indonesia, being the largest player, changed its stance to become self-reliant and banned nickel ore exports to other countries for enrichment in 2014.

- Nickel output has increased in recent years. Mainly because of the demand from the EV sector, with 2 of the 5 most popular EV battery chemistries using nickel.

Source: USGC, LME, Nickel Institute, ISSF, Reuters

Source: USGC, LME, Nickel Institute, ISSF, Reuters

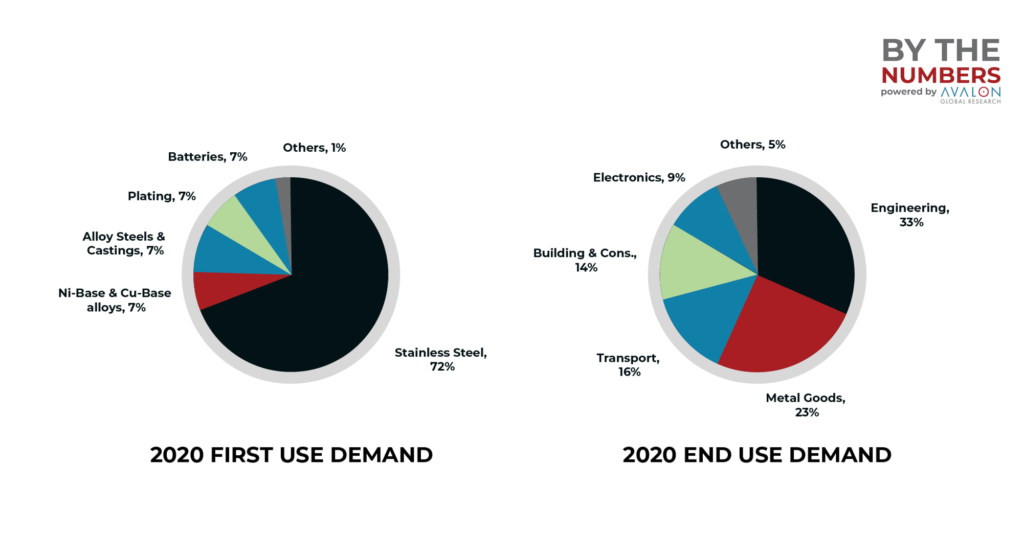

Stainless steel drives the demand

- Stainless steel output has seen a rise in the past 5 years, with 2021 production witnessing 11% YoY growth. Stainless steel is likely to remain the leading nickel consumer in the short-term, accounting for a 72% share in nickel consumption in 2021.

- While the stainless steel output is expected to rise moderately, the nickel demand is estimated to grow more rapidly because of the additional demand from EVs & energy storage with many countries increasingly announcing electrification and emission reduction targets.

- Meanwhile, Japan’s biggest smelter Sumitomo Metal expects the demand for nickel, used in batteries, to rise 20% in 2022.

- New Indonesian projects may offset the increasing demand in the short to mid-term.

Substitution to nickel: LFP in EV batteries

- A potential substitution in EV batteries is Lithium-Iron-Phosphate (LFP) battery chemistry, as it is significantly cheaper and safer to use.

- While several OEMs already use LFP batteries currently, a surge in nickel prices can push other makers to start using LFP batteries too, or develop other chemistries which are not dependent on nickel.

- However, apart from substitution in EV batteries, there isn’t a viable alternative to nickel, especially in the other end-use sectors at present.

Source: USGC, LME, Nickel Institute, ISSF, Reuters

Source: USGC, LME, Nickel Institute, ISSF, Reuters

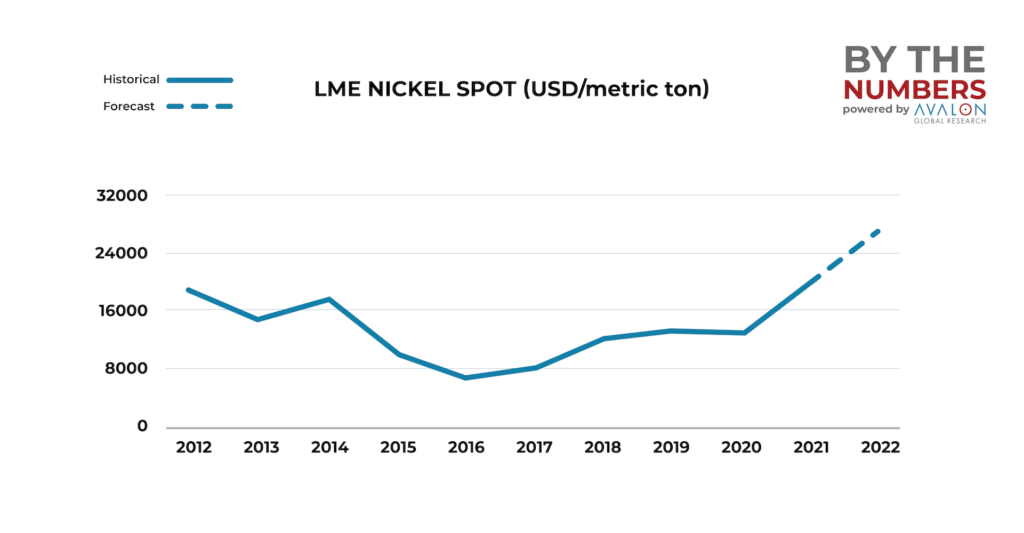

Mid-term & long run price forecast – The AGR analysis

Source: Nickel Investing News, USGS, Nickel Institute, Reuters

Source: Nickel Investing News, USGS, Nickel Institute, Reuters

Price forecast bullish amid higher demand rebound and EV boom

- Short-Term Forecast

- Upside factors: Strong rebound in the nickel demand post Covid-19 pandemic from EVs; nickel pig iron (NPI) supply constraints in China amid import duties on Indonesian stainless steel.

- Downside factors: Commissioning of China-based Jinchuan’s new 100 Ktpa nickel sulphate plant can offset the additional demand.

- Medium Term Forecast (1 to 3 years)

- Upside factors: Government announcements to cap emission reduction, resulting in electrification and correspondingly higher nickel demand.

- Downside factors: Alternate battery chemistries like LFP; Indonesian nickel sulphate and NPI expansion; battery recycling and scrap gains, reducing nickel dependency.

The Russia-Ukraine war impact

The 2-fold impact of the Russia-Ukraine conflict

Increased LME prices & decreased SHFE prices

- The ongoing conflict between Russia (the 3rd largest nickel producer) and Ukraine has so far resulted in both LME & SHFE prices going up.

- As the conflict escalates, and European countries announce to cease nickel imports from the Russian firm Nornickel, the supply could be shifted to China.

- This will cause the LME price to be upward of US$ 21,000/t due to supply restriction and high demand from the global energy transition. However, SHFE prices would be lower due to ample domestic supply.

Premiums widen by region and brand

- Meanwhile, disruption in the trade flows will cause spot premiums to vary by region globally, and the difference in premiums among different brands will also increase.

Our View

AGR estimates the prices to start settling around June-July, from the all-time high of ~48,000/t (in early March this year), and end 2022 between $26,000-27,000/t.

We expect the prices to decrease further (beyond 2022) because of additional supply coming in from Indonesia, with the medium term prices hovering around mid $20,000/t.

AUTHORS –

Neetishwar Jha, Analyst

Business Analyst with over 3 years of experience in researching, collecting & interpreting data to extract key insights and influence business decisions. Specializing in metals, mining, EVs and logistics.

Ankur Rastogi, Vice President

Seasoned management consulting and business research professional with over 12 years of experience, focusing on client acquisition and key client management and project execution, mainly in metals & minerals and Energy verticals.

The Metals, Minerals, and Mining Research Team

Our Metals, Minerals and Mining Market Research Team understands the dynamics of the value chain and global trade very well and has conducted numerous studies in both ferrous, non-ferrous metals and minerals. To know more about the practice, please visit Metals, Minerals, and Mining.

About Avalon Global Research

AGR Knowledge (AGR) is a specialist research, analytics, and advisory firm that helps clients with custom knowledge solutions to identify and realize global market growth opportunities, partnerships, and potential investments.

AGR helps address complex business challenges and enables informed decisions with its wide array of research and knowledge services for its clients across diverse industries, such as Energy, Engineering, Healthcare, Food & Agriculture, and Logistics, in over 100 countries.