2022 was a challenging year for gold. Despite the Russia-Ukraine war, geopolitical upheavals, rising inflation, and global economic turmoil, gold remained almost flat through the year. The precious metal’s lacklustre price performance caused a further build-up of negative sentiment. Although gold continues to face some challenges, there is a developing beliefitcould outperform in 2023. Some other factors that could drive gold prices higher are given below.

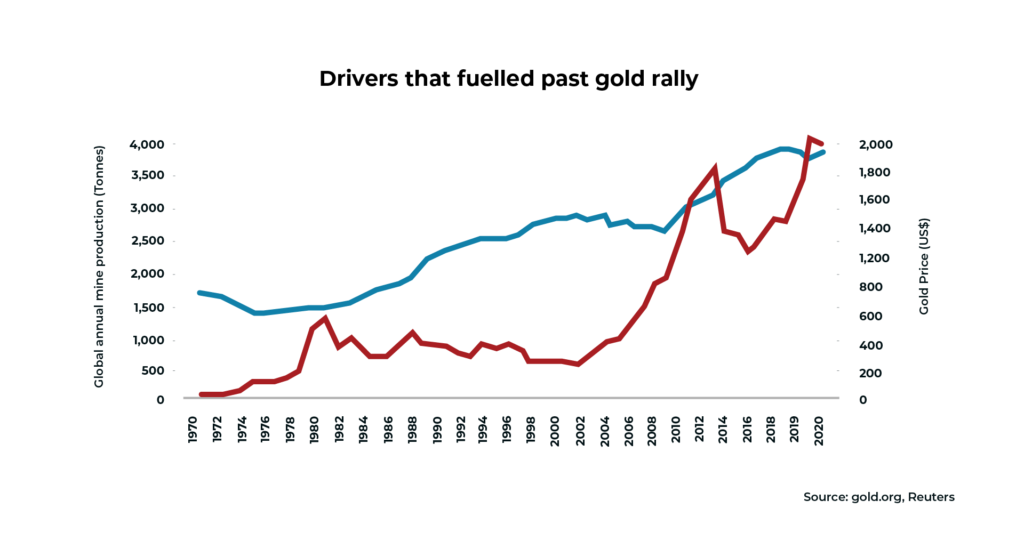

Drivers that fuelled past gold rally

As depicted in the chart below, there were two major gold bull markets over the past 52 years. End of the Bretton Woods agreement in 1971 gave rise to a roaring bull market: gold was 17x higher in a decade to US$586 an ounce in 1980. Likewise, there was another sharp rally in 2012, with the metal reaching US$1,674 and surpassing the 2000 level by 6x. Though various factors triggered substantial price action in gold, one common theme was the considerable decline in global production during the period that, in turn, played a significant role in deciding intensity of the gold rally.

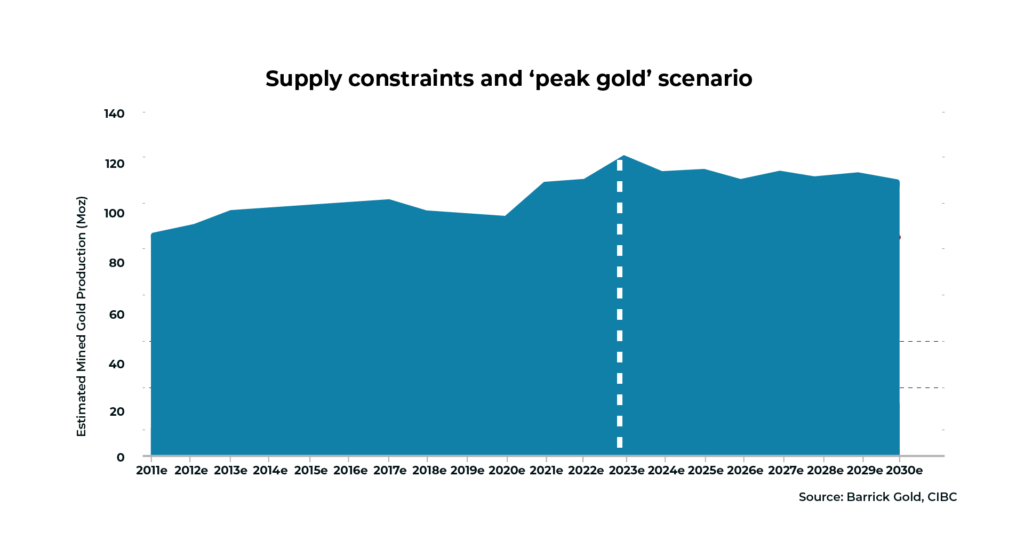

Supply constraints and peak gold’ scenario

A similar macro trend seems to be playing out in the current scenario. Global gold production has been falling since 2018 and is likely to continue the downtrend. Some experts believe the world has reached ‘peak gold’ or a stage where the maximum rate has been achieved in global extraction and that even a huge spike in prices cannot impact production.

According to the Australian government’s Department of Industry, Science, Energy and Resources (DISER), after a peak of 3,807 tonnes in 2024, the world’s gold mine production is projected to decline at an annual rate of 0.8% in 2025 and 2026 to 3,746 tonnes in 2026. This has been ascribed to declining ore grades and increasing operational costs. The report also mentions the number of unprofitable gold mines is expected to rise from 5% in 2021 to 10% in 2026. As a result, there is likely to be additional gold mine closures and lower production during the same period.

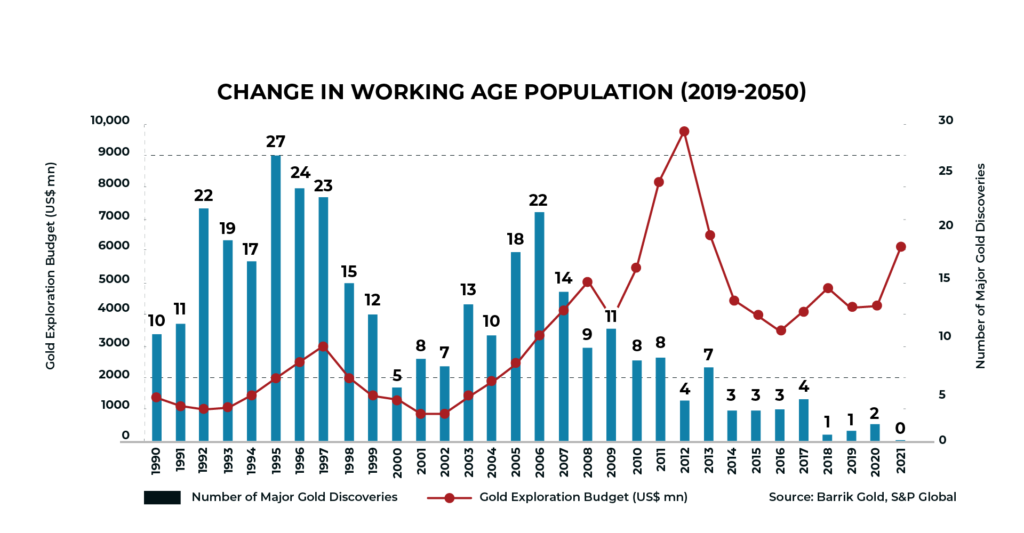

Lack of major discoveries

New gold discoveries have been falling consistently over the last few years despite higher exploration budgets (refer to chart below). While discovering gold is becoming increasingly difficult, there has been a decline in the grades of ore bodies as well. S&P Global Markets estimated more than 329 gold deposits were discovered between 1990 and 2020, but just 29 were located in the most recent decade.

Focus on green agenda

Miners are redirecting capital from gold-focused projects to battery,metals and other mineral resources for adopting greener alternatives and complying with the climate change agenda. In fact, several gold-focused miners have witnessed significant decline in production. For example, Barrick Gold’s production dipped 43% since 2010, while that for AngloGold Ashantideclined 45% during the same period. Similarly, Newmont Corporation and Kinross Gold witnessed a substantial fall in production. Such constraints magnify the bullish, long-term investment case for precious metal.

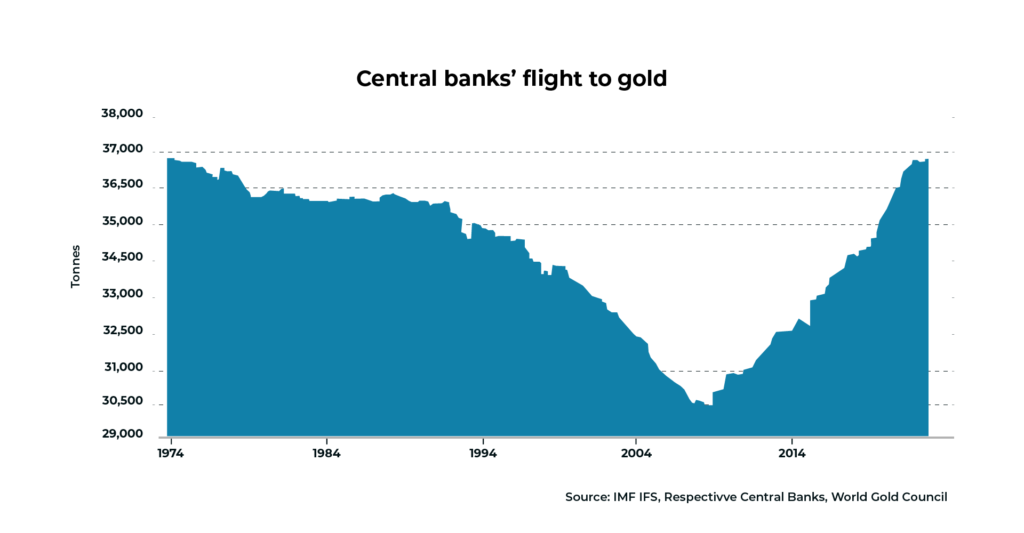

Central banks flight to gold

Global central banks started stockpiling gold at a frantic pace in 2022—a trend that has not been witnessed since 1967 (ft.com) when the dollar was still pegged to gold. On the other hand, China and Russia have been incessantly increasing their gold reserves. While China’s gold reserves increased 85% to 1,948t during 2010-2021, that of Russia surged 192% to 2,302t. Moreover, demand from other emerging nations has been inching up, with major accumulationsbyTurkey (103t), Thailand (90.2t), Japan (80.76t), India (77.45t), Uzbekistan (37t), Qatar (31t), Kazakhstan (18t) and the UAE (18t)in 2022.

The next few quarters will decide whether the gold-buying spree of central banks was an opportunistic one, to capitalise on lower gold prices, or a structural shift. In all likelihood, reserve demand for central banks may continue to grow amid global macroeconomic uncertainty and efforts by China and other nations to find an alternative trading currency.

Conclusion

Gold is expected to remain robust due to higher global uncertainty and a dovish Fed, which is likely to weaken the USD, boosting demand for the safe-haven precious metal. Additionally, inflows into gold ETFs might start gaining momentum as the Fed is likely to start approaching the final leg of rate hikes in the current cycle. These factors, coupled with the points discussed above, could ensure sustained demand for gold, going forward.

Author: Pravin Bokade, Director- Investment Research