The global economic crisis of 2008 that shook financial institutions worldwide highlighted the vulnerability of economies to manipulation of data and withholding of information by market participants and customers. Fourteen years down the line, we are at a cusp again where we need to ask a fundamental question, especially as we emerge from the havoc-wreaking COVID-19 pandemic and in the light of rapid digitalisation—are our institutions safe from unethical handling of data?

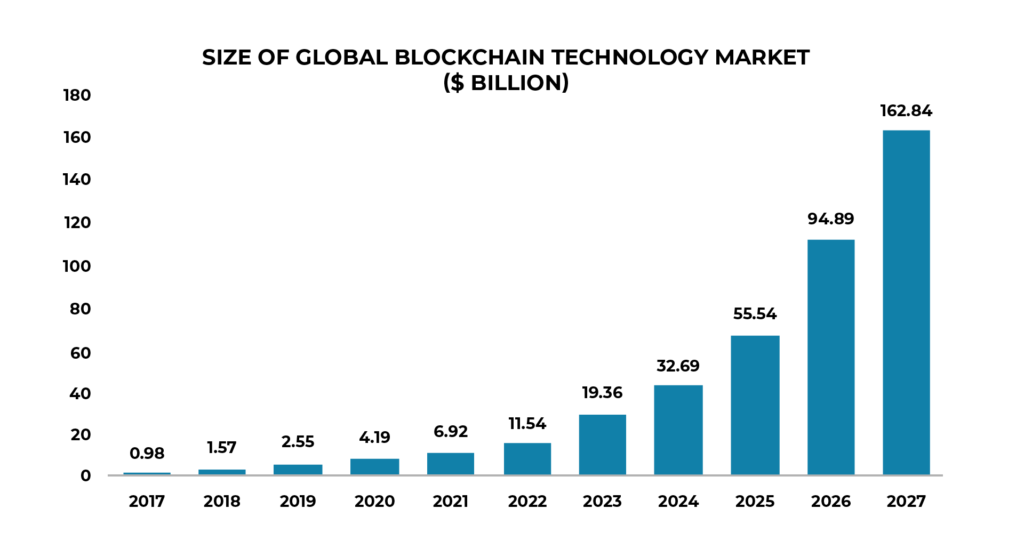

Perhaps, yes; only that this time, hopes are riding high on technology, which is revolutionising the financial landscape. One such breakthrough technology is blockchain with the immense potential to disrupt business models and financial institutions. What makes blockchain so disruptive is that it is capable of transforming business practices and enriching the finance industry by facilitating the development of new business models. No wonder, then, the market for blockchain technology, estimated at $6.92 billion in 2021, is projected to reach $162.84 billion in 2027.

What is blockchain? How does it help retail banking and facilitate financial inclusion?

A blockchain is a distributed ledger technology (DLT) with multiple ledgers and points of entries (to those with authority). It can store metadata in blocks, thereby enabling network-based consensus for numerous transactions simultaneously.

In contrast to the traditional methods of storing data that are centralised, expensive, and inefficient, blockchain paves the way for decentralisation of data among various stakeholders, which facilitates peer-to-peer (P2P) transactions on the network. Moreover, the blockchain database is immutable—the information is indelible and the history of the transactions cannot be changed. Furthermore, as data is stored in nodes, or a ‘block’, and every block is connected with the other, it simplifies the transfer of information and ensures transparency. Moreover, the transactions are end-to-end encrypted and, therefore, highly secure.

Most important, the pandemic has significantly changed the way businesses function, catapulting data to the centre—it is now considered more valuable than oil. Against this backdrop, there is ample scope to widen the application of blockchain. It can be integrated with Big Data to develop data-based solutions in banking and to boost financial inclusion.

Trust is the most critical component in any business trading or financial transaction. Leveraging blockchain, FinTech players are looking to build trust among consumers. Blockchain eliminates the role of intermediaries by facilitating transparency and smooth transfer of assets, speeding up transactions, and ensuring security of data. Interestingly, the ‘intermediaries’ are none other than the retail banks. As the heat from FinTech organisations with expertise in blockchain turns up, it is raising potent questions around the survival of these retail banks that have so far remained aloof to shared electronic ledger—and consequently behind in the race. In their bid to gain an edge over other FinTech incumbents, a few retail banks are actively working to integrate blockchain in their operations and processes. Bank of America (BoA), for instance, has won nearly 35 patents for advancements in blockchain technology. Other competitors such as Barclays, Citibank, Goldman Sachs, and UBS are now using the R3CEV consortium to explore its potential in reducing cost and achieving unrealised efficiency (Chang et.al, 2020). Lastly, JP Morgan, HSBC and others have successfully executed transactions via blockchain, taking book-keeping, managing accounts and storing ledger accounts to a different plane altogether.

Considering the use of blockchain as listed above, the technology is set to play a crucial role in accelerating financial inclusion – the core of economic development. According to the World Bank, as of 2017, 1.7 billion people globally were unbanked (constituting up to 20.6% of the global population), while 2.8 billion were underbanked, highly vulnerable to economic and other emergencies. Blockchain can help address the challenges associated with the delivery of affordable financial services, thereby increasing their usability. Implementing the technology will eliminate the transportation and operation costs related to gaining access to traditional financial institutions. It can also simplify processes across the spectrum—something as easy as setting up an account or as complex as claiming insurance money can be done using a smartphone.

This article provides a detail overview of the impact of blockchain in the retail banking sector and its role in financial inclusion, and, based on it, the road ahead.

1. Cross-border payments & remittances

Banks and most financial institutions globally use SWIFT to transmit information such as that related to money transfers. This is a lengthy and costly process, consuming 1–5 business days on an average, with the cost of transaction averaging $40–50. As per estimates, cross-border payment flows globally are expected to reach $156 trillion in 2022, expanding at a CAGR of 5% over 2018–22. The growth potential notwithstanding, the overall process is unwieldy and lacks transparency. Thus, to facilitate P2P transactions, improve their efficiency as well as speed (by eliminating intermediaries and other hassles), and to make them cost-effective, banks are increasingly integrating blockchain technologies. According to a 2019 McKinsey report, applying blockchains to cross-border payments could yield $4 billion in savings annually. Retail banks are also developing the Interbank Information Network (IIN) as part of their blockchain initiative to simplify regulatory compliance and minimise the number of intermediaries in transaction. Thus encouraged, these banks are now working to expand the application of blockchain from fiat money to crypto-based asset transactions globally.

Traditional money exchange providers charge high rates (in percentage terms) even for smaller transactions; this will deter financial inclusion, instead of boosting it, even if a person were to get the opportunity to access these institutions. Blockchain, on the other hand, facilitates low-cost, traceable transactions in multiple currencies in wallets across mobile networks globally. It also enables ‘smart’ contracts that are automatic and secure, thereby saving transportation, maintenance, and other related costs. Given these benefits, blockchain is an effective tool to crack the problem of poor access to financial services.

2. KYC/KYB

It is mandatory for all retail banks to comply with KYC and KYB norms during customer onboarding, as part of identity verification protocols. It helps in effective risk management and personalisation of services. According to published research, banks lose $15–20 billion annually due to identity-related frauds. Despite their significance in preventing fraud, KYC/KYB processes are often frowned upon because they are inefficient at most places, tedious, time-consuming, and labour-intensive. Regular updates are required in line with changes in regulatory requirements and information. Plus, manual documentation is prone to errors and frustrating for consumers too. Blockchain, which entails bringing data on a decentralised network, coupled with authorised storage and access, can help in eliminating the inefficiencies associated with manual processes and avoid duplication of effort. Moreover, it can improve privacy as consumer information is stored in smart contracts and transactions can be tracked as and when required.

Blockchain-enabled KYC/KYB can play a key role in boosting financial inclusion. Paper-based identification or documentation is an important factor behind the exclusion of millions who do have the wherewithal to furnish the proof of their identity. One of the countries leading by example in this regard is Estonia. It has implemented a national digital identity scheme using blockchain. This includes providing citizens with Estonia ID cards and mobile ID cards that are cryptographically encrypted and unique, all registered on a common blockchain. This ID card allows people to access public and financial services along with medical and emergency services.

Thus, switching to digital identification while upholding the standards for security could contribute to inclusive growth.

3. Risk and asset management

Often, consumers have multiple accounts in more than one bank and simultaneously avail of financial products offered by various financial institutions. Because of system integration (as no institution works in abject isolation in a digitally connected world), capturing data across the financial network, especially during buying and selling of assets, could be highly frustrating. Additionally, asset management requires efficient profiling of consumers, assessing their preferences, ability to take risks, etc. — all these activities centre around obtaining and working on data stored across various financial institutions. Blockchain can address this issue due to decentralised storage of information. Only pertinent data can be extracted for personalised asset management recommendations and investment profiling, which increases both efficiency and accuracy.

Settling accounts in asset markets is highly time-consuming due to the existence of poor channels for transfer of funds or assets and presence of intermediaries. Blockchain can help in making the process more efficient, transparent and cost-effective. Banks can also save billions of dollars by using blockchain technology in the asset market. Furthermore, the personalisation of assets and risks will facilitate financial inclusion.

4. Insurance and credit rating

Ever since the subprime mortgage crisis, banks are treading cautiously in disbursing loans to consumers. Adopting a conservative approach, they are following new rating models to assess creditworthiness, which requires collation of information from other financial institutions and banks. Blockchain can help address the inefficiencies associated with traditional credit rating mechanisms, such as insufficient information or misinterpretation or biases. The technology, with decentralised finance at its core, provides holistic information from the required multiple parties to facilitate credit lending decisions. Thus, credit scoring is decentralised, performed through various lenses, and is therefore more reliable and effective. Bloom and PayPie undertake credit scoring using blockchain accounting.

Almost a third of the world’s population engages in small to minor transactions. As a result, it is difficult to analyse their credit history and accordingly determine credit worthiness. The International Finance Corporation (IFC) estimates that almost half of micro, small, and medium enterprises in developing countries have an unmet credit gap of $5.2 trillion every year. Projects such as the Grassroots Economics, funded by UNICEF’s Innovation Fund, are aimed at providing credit for transactions based on blockchain technology; these are backed by atypical collateral that include livestock, crops, and other physical assets.

Lastly, insurance agencies often face challenges in the form of adverse selection. Here, blockchain can come to rescue by opening up channels for information and bridging the gap for various stakeholders. Moreover, the seamless, technology-based user-friendly interface, where data is stored in the block, eliminates bottlenecks such as documentation. It helps in promoting integration and makes it easy for insurance companies to obtain information.

Some of the areas where blockchain can, therefore, help are online underwriting, improvement of supervision, prevention of money laundering and addressing issues pertaining to risk control mechanisms.

Scope and the way ahead

Blockchain is a developing technology, still in an experimental stage. With digital recording of information at its core, it could certainly prove transformative and disrupt traditional retail banking and financial functions, especially by making them cost-effective, efficient, user-friendly and secure. Perhaps the biggest impact of this disruptive technology will be in paving the way for financial inclusion in developing countries.

That said, as with any technology, blockchain has its own fair share of issues. First, it is vulnerable to hacking, especially transactions at certain stages in cryptocurrency trading. Second, concerns arise from the unprecedented growth in the size of blockchain. This could mean that a lot of it is yet to be tested and proved, besides, of course, the greater scope for privacy issues. This calls for having a strong cyber security mechanism in place. Last but not the least is the need for regulations. Governments need to come up with rules of engagement and laws that protect consumers from fraud.

At the end of the day, if we are talking about blockchain as a way to pre-empt and prevent financial crises born of manipulation of data and unethical practices, we have to ensure that blockchain has the trust of consumers. No FinTech innovation will make sense if it cannot win consumers. To build credibility in a technology that is still taking shape, the onus lies equally on policymakers, institutions and consumers. While tech firms/financial institutions and policymakers need to work in collaboration to build a resilient infrastructure to prevent misuse of the technology, consumers must also stay alert, aware of the latest developments and most of all not fall prey to trends and publicity.

Author –

Prasanth Radhakrishnan, Associate Director, Avalon Global Research

Contact us at https://www.agrknowledge.com/contact-us