In this article, we elaborate on key factors likely to drive demand for copper in the coming decade and the commensurate supply-side challenges. Based on the resultant deficit, we build a case for an upbeat scenario in copper prices over the next few years.

Doctor copper

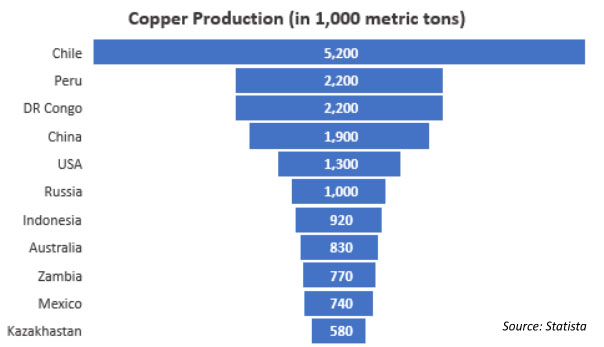

Copper is the third most widely used metal worldwide, mainly across industries. The metal is also called Doctor Copper due to its ability to predict the global economy’s health. Among countries, Chile is the largest copper producer in the world, followed by Peru, DR Congo, China and the US. On the other hand, China is also the largest consumer and importer, followed by Japan, India, South Korea and Germany.

Net-zero goals driving demand

As the world has started shifting from fossil fuels to renewables, demand for certain metals, including copper, is expected to rise manifold in the next decade. Electric vehicles (EVs), wind farms, solar energy and extra high-voltage (EHV) cables will be major demand drivers as the intensity of copper usage in these technologies is significantly higher. For example, an electric car consumes around 4x (~80 kg/car) more copper than combustion cars (~18-20 kg/car), while a solar plant uses around 9,000 pounds of copper per MW of peak capacity (source: Solar Industry Magazine). Similarly, wind farms require 5,600-14,900 pounds of copper per MW, with offshore wind farms needing ~21,000 pounds per MW (source: Copper Development Association).

Supply shocks

While demand for copper is rising steadily, supply has not been in tandem. Challenges, such as internal upheavals, operational inefficiencies and regulatory disagreements, are disrupting production across large producer countries (Chile, Peru and DR Congo). Other primary reasons for supply constraints have been chronic underinvestment in copper mining, lack of exploration projects, declining ore quality across most mines (best ones already mined), and rapid adoption of ESG standards. These factors could further slowdown investments in new projects amid the current high interest rate environment.

Peak production

Establishing a new mine is a highly capital-intensive task, and copper is a long cycle commodity. It takes around a decade to ramp up production due to numerous challenges such as infrastructure bottlenecks, environmental concerns, rising exploration costs, and regulatory issues. As a result, existing copper miners will have to do most of the heavy lifting for fulfilling current demand. Alternatively, this could imply the current scenario is likely to be the peak in copper production.

Looming deficit

With demand for copper rising firmly, due to net-zero emission goals, and supply remaining weak, miners are predicting a shortfall in the coming decade. Fastmarkets estimates a deficit of 6 million tons by 2030. As per Bloomberg NEF, the mined-output gap will likely reach 14 million tons by 2040. On the other hand, Goldman Sachs projects an 8-million-ton deficit in the coming decade; in addressing this deficit, miners are expected to incur a whopping USD150bn in capital expenditure.

Codelco, a state-owned Chilean mining company and one of the largest copper producers worldwide, believes the gap will reach 8 million tons in the coming decade. A report from S&P Global estimates world demand to reach 53 million tons in 2050, more than the entire copper consumption on a global scale over the last 120 years.

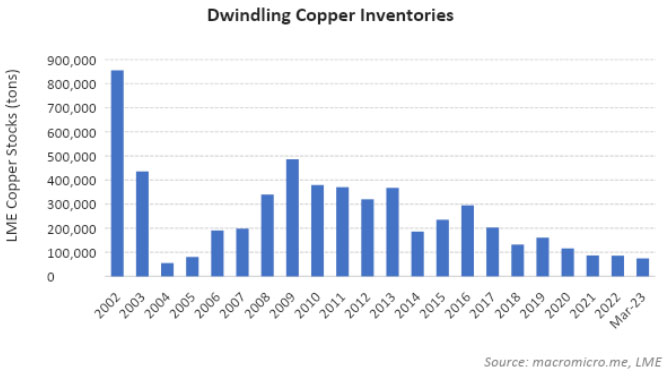

Inventory levels serve as an important indicator of demand-supply dynamics. In the case of copper, they have changed dramatically over a longer time frame and are at the lowest level since 2005. Declining inventories also reflect more profound changes currently occurring in the market and, ultimately, if not immediately, could severely impact prices. Trafigura predicts copper prices will scale to a new all-time high in the next year, reaching US$12,000 a ton. On the other hand, Goldman Sachs expects the world will run out of visible inventories by September 2023 and prices could reach USD$10,500 a ton in the near term from USD8,930 a ton currently. The long-term target is $15,000 per ton, almost 70% upside from the current level.

M&A spree unlikely to address demand concerns

As copper is expected to be in short supply and new discoveries are elusive, large copper miners seek inorganic growth opportunities. BHP plans to acquire an Australian copper-gold producer, Oz Minerals, for USD6.6bn, while Rio Tinto increased its stake in Mongolia’s Oyo Tolgoi copper mine. In a latest transaction, Canada’s Lundin Mining Corp acquired a majority stake in Chile’s Caserones copper mine for about US950mn. Though inorganic expansion could help ramp up production of acquirers, it cannot address industry-wide supply issues.

Conclusion

Copper is a critical commodity for meeting clean energy goals, but is in serious short supply. However, demand has been rising consistently due to decarbonisation initiatives. Maximising copper production is crucial for addressing the structural change in demand. Copper prices are likely to soar in the coming years unless new supply comes online.

Author: Pravin Bokade